[ad_1]

Thomas Barwick/DigitalVision through Getty Photographs

Vacation + Leisure Co. (NYSE:TNL) has been working with challenges in excess of the earlier few of several years, thanks to COVID-19 pandemic and risky need dynamics in the hospitality sector. As the economy reopened so also did Journey + Leisure’s organization but points appear established to stall once again. Investing in timeshare firms at the starting of a new enterprise cycle can often supply alternatives for substantial returns. Timeshares are a very cyclical market so it works the two means. In downturns, luxury massive-ticket products like timeshares get hit the most difficult but the rebrand to Vacation + Leisure gave Wyndham Places a number of new tools to aid the corporation cope throughout tricky times like these. Right now we’re heading to get a look at some of the most current resources and see how they could be benefiting buyers in the near potential.

The Product or service

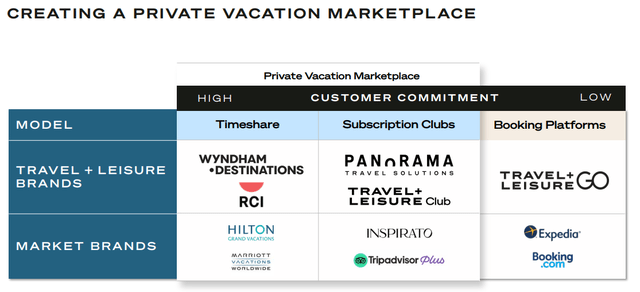

Vacation + Leisure is still a timeshare enterprise, but their exclusive acquire on the product or service differentiates them. Instead of a traditional timeshare, Vacation + Leisure sells getaway clubs. Members can layout their personal vacations and they can use their possession in a amount of means. It was the Iphone minute for Vacation + Leisure. They also nevertheless get servicing charges for their timeshare choices which is a handy kind of passive earnings. This permitted the enterprise to emphasis on constructing a potent portfolio rather of getting and marketing a single choose site at a time.

Having a robust hotel portfolio is expensive and makes a big barrier to entry for competitors as they have to go up against an full fleet of accommodations vs . just a single beautiful area and the TNL portfolio features some 245 places in some of the most beautiful places.

Journey + Leisure

As a outcome, the benefit of timeshare stocks depends mostly on the range of goods and spots they give. Getting a deep site catalog would make it more durable for levels of competition to poach buyers and is a big offering point for new buyers. It also gives shareholders assurance in the firm’s means to keep current customers. Travel + Leisure has accomplished effectively creating up its catalog.

Vacation + Leisure also has the RCI Exchange that facilitates the buying and selling of timeshare- and it truly is a single of the world’s greatest by volume. They are fundamentally a one particular-halt shop for all things timeshare and it generally seems to be involved in any ground breaking answers in the room.

Some queries have been raised about the timeshare industry’s potential to catch the attention of millennial funds, but there are some efforts underway that should enable it make improvements to. Travel + Leisure commenced presenting membership products and services to millennials who usually are not as likely to dedicate to a prolonged-time period expense. The introduction of Panorama’s subscription providers could be pivotal for Travel + Leisure, especially in light-weight of current opposition from Airbnb and other quick-expression lodging products and solutions. Membership expert services could pretty nicely end up getting the subsequent frontier in the timeshare market.

Travel + Leisure

Potent Gross Margins Post Restoration

Thanks to an enhanced value proposition relative to greater hotel charges and powerful work figures, TNL’s upcoming outlook is searching promising.

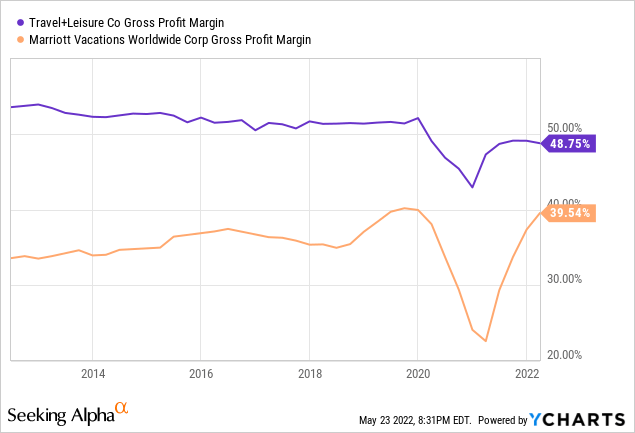

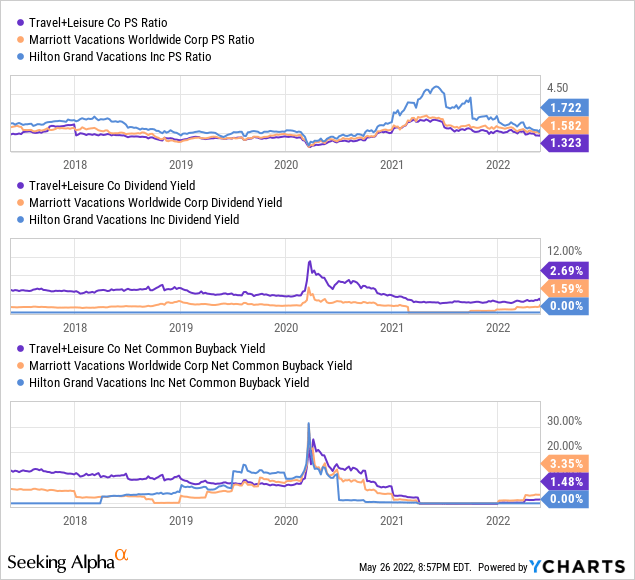

The business enjoys sturdy gross margins thanks to pricing electrical power but they have been declining. The Wyndham Destinations offerings exist at the medium stage of the pricing spectrum. In comparison to far more magnificent offerings like the Marriott Vacations clubs, you would hope Vacation + Leisure’s offerings to have considerably less favorable margins but they truly outperform.

This is actually a testament to the organizational effectiveness of the leadership group. Selling prices have been able to balance out the costs, major to better revenues. Regulate about servicing agreements and a stable fee-based mostly design allow the enterprise to properly move on expenses to consumers.

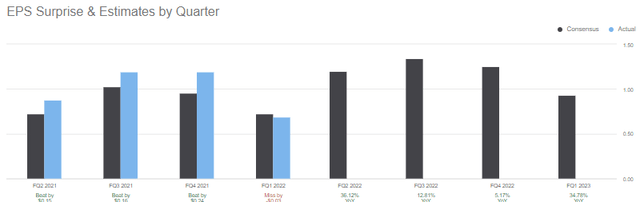

The recovery has seriously taken root for the business. EPS traits have been favorable right until not long ago. The organization has a cyclical component to income and has a short while ago been beating estimates for the most aspect.

Trying to get Alpha

Most notably in their family vacation ownership enterprise, the firm had an regular VPG (volume for every guest) of $3,377 in Q1 is increased than at any time right before for the organization and 40% above last year’s quantities. It is also crucial to don’t forget that inflation is good for their corporation. Charges for resorts and getaway houses are climbing. This assists include value to the timeshare notion for shoppers as it results in being a lot more value-helpful relative to being in other forms of lodging. Interest premiums soaring on the other hand are extra relating to.

Terrible Circumstances for Cyclical Performs

Reviews from the Federal Reserve advise that we are heading to charge hikes between 3-5 periods this yr. This will be the to start with time fees have amplified because the start of the pandemic-induced lockdowns and it could influence financial growth and fairness prices. What is actually additional, there is a inclination in the timeshare market to finance purchases so a prolonged period of greater fees will increase the all round price tag of VO solutions to the consumer.

Very long-phrase traders who preserve their eyes open must have a lot of possibilities if they continue to be diversified. The market place has been finding additional unstable as premiums rise and points get tenser abroad.

They influence the volatility of stocks and their multiples. When interest charges are large, shares are significantly less appealing because they supply reduced returns.

The hospitality market is just one of the most affected by curiosity charges because providers have a tendency to have a large personal debt-to-equity ratio.

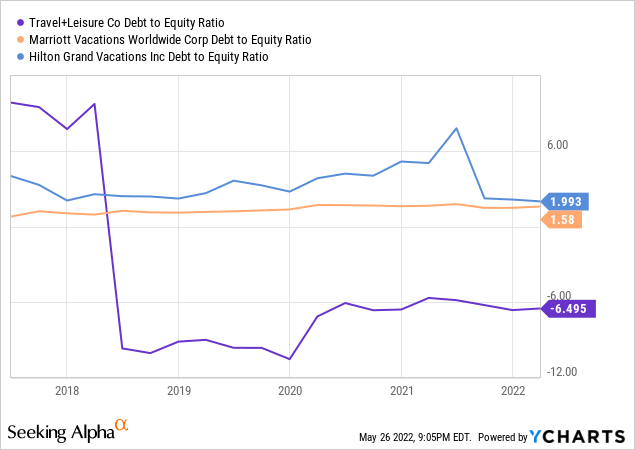

This indicates that when fascination prices go up, so does the charge of borrowing revenue for these businesses. This puts timeshare organizations in a difficult location. They have to pay a lot more to borrow money simply because of the fascination premiums. They are inclined to stay clear of this by building somewhat steady agreements with fixed fees for revolving traces of credit history. This is in which Journey + Leisure stands out towards its peers. They have almost no credit card debt and no urgent require for liquidity injections. It is most likely that they may possibly safe credit rating to beef up the equilibrium sheet if the economy was to go south in a major way but the organization has accomplished these kinds of a fantastic task handling its liquidity and over-all value of funds that this sort of a move must be immediately forgiven if it had been to take place.

There is also the simple fact that a economic downturn is not all doom and gloom for much larger working experience players like Journey + Leisure. There is generally home for vital acquisitions at beneficial charges and Wyndham has performed some wonderful discounts in the past. Travel + Leisure is an outgrowth of the Wyndham model but it will be exciting to see if they can have identical results in the event of a downturn.

Conclusion

Travel + Leisure is fairly valued ideal now. We could be going into a big slowdown and they get in touch with hospitality a cyclical enjoy for a explanation. I am by no means heading to propose obtaining a timeshare inventory on the cusp of a economic downturn but there is a lot to love about Travel + Leisure in this article. The inventory has bought off a ton but it could nevertheless go reduced. I wouldn’t be in a hurry to purchase just but but I see no rationale why investors should hurry to element with their shares at this amount. I amount the stock as a Hold.

[ad_2]

Supply hyperlink

More Stories

National Park Adventures: Find Hidden Gems in the Wild

National Park Adventures: Explore Majestic Landscapes

Journey into the Wild with National Park Adventures