[ad_1]

amriphoto/E+ via Getty Images

Thesis

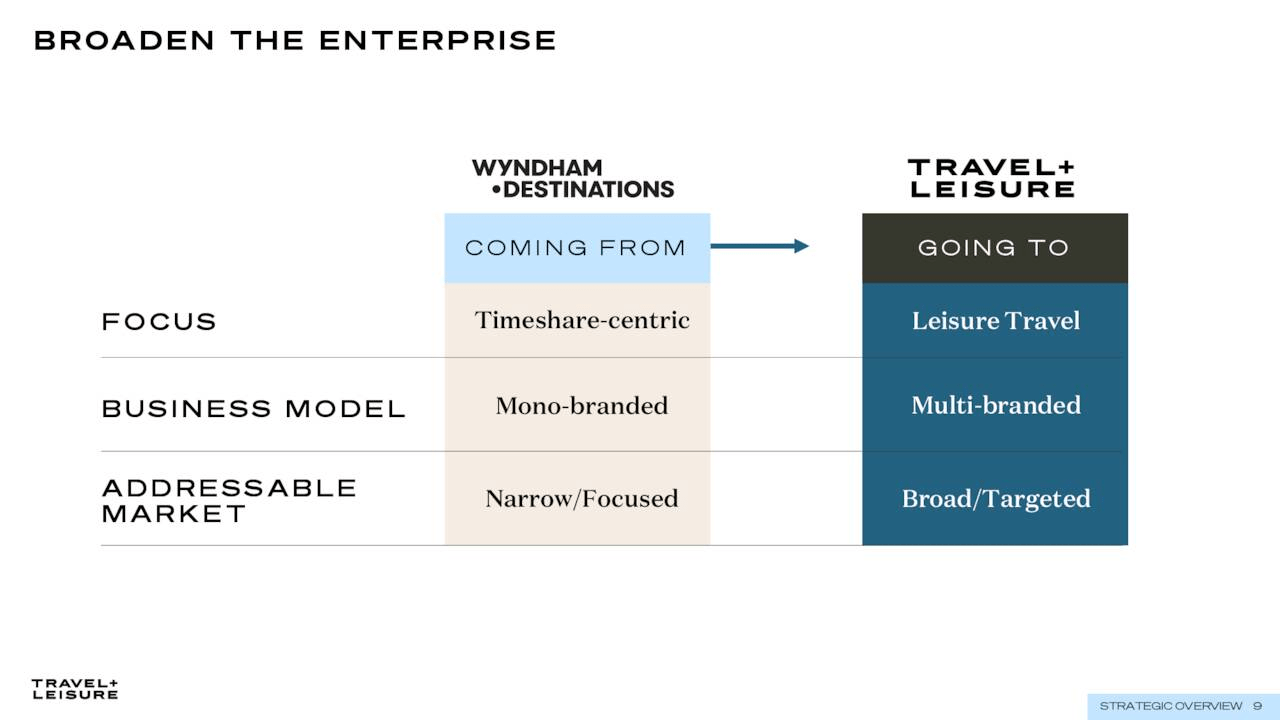

Travel + Leisure (NYSE:TNL) is quite an interesting new conglomerate in the travel industry. Formerly part of Time Magazine owner Meredith Co (GTN)(IAC), T+L the magazine was acquired by Wyndham Hotels (WH) spin-off Wyndham Destinations, which are primarily timeshare resort operations, but Wyndham took the famous magazine’s name. The goal of the acquisition and rebranding under the T+L banner was for multiple reasons. First, move away from negative timeshare stigma due to rights and cost. Second, increase visibility of the platform under one banner. Third, increase operational efficiency through integration, all while increasing customer base. The companies are now able to work together, rather than alongside each other, and management expects these synergies to drive growth and profits.

I expect the results to be favorable, but there is plenty of competition in the “lifestyle travel” segment, such as Airbnb (ABNB). As investors, it will be important to choose parts of the industry that are currently weak, but offer upside potential as performance returns to form. The uncertainty around TNL offers a steep undervaluation all while synergies between operating units will allow the company to outperform. While financially the jury is still out, the investment is certainly worth consideration over the next few quarters thanks to the favorable valuation.

TNL

The New Travel + Leisure

Prior to merging, the two separate entities were highly specialized, one a timeshare provider and the other a travel magazine. With print media taking a hit over the past few decades, perhaps as a result of declines in political interest, Travel + Leisure invested heavily into their online platform. Also, the brand continues to offer yearly award rankings of the top hotels, destinations, and regions of the world. The publication is often rated as the top quality name in the industry and has earned plenty of fans the world over. Altogether, if travel popularity increases to levels seen prior to the pandemic, T+L is set to grow with the market. On the other hand, timeshares are a different story as their financial viability and popularity wanes over time, especially with steep competition from vacation rentals and traditional hotel/motel.

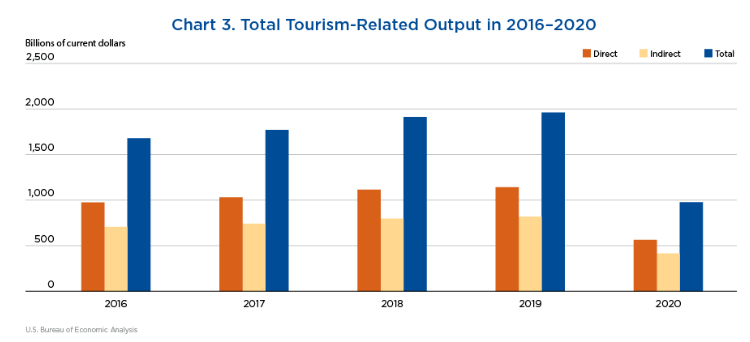

USBEA

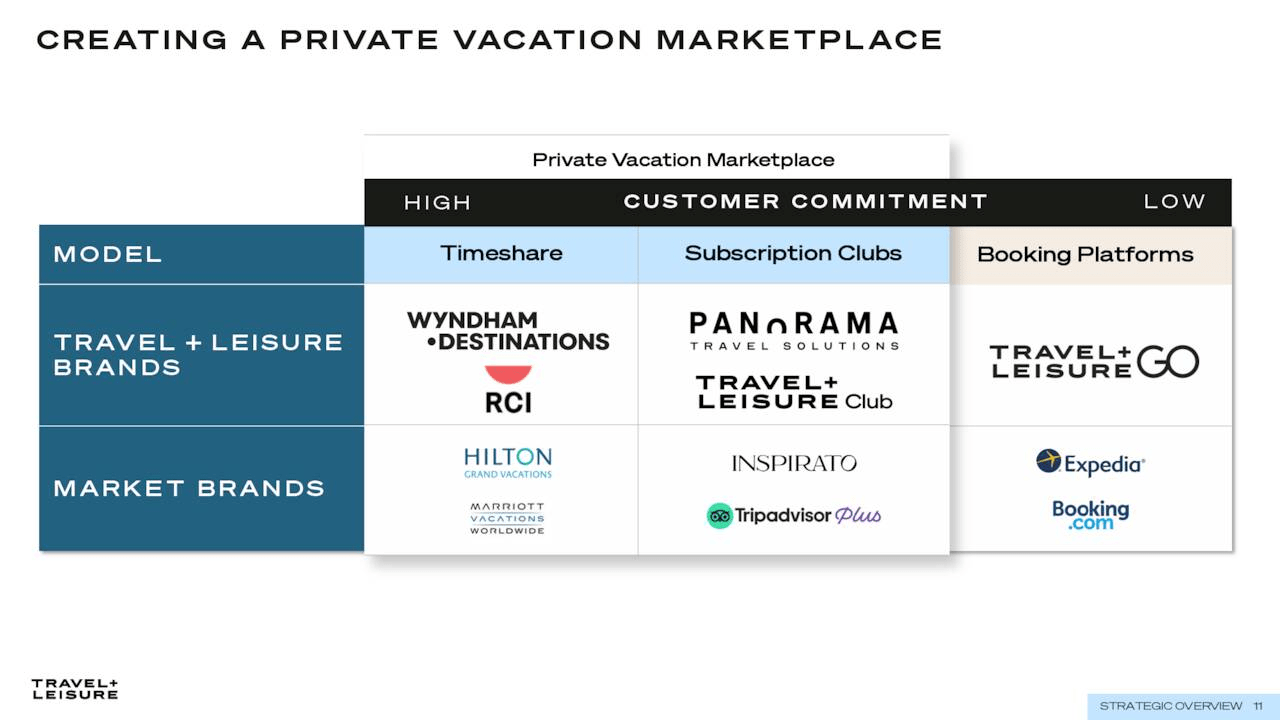

To tackle some issues, the company is shifting business strategies, opting to go with the popular subscription model. This includes the various Wyndham Destinations Clubs, Travel + Leisure Club, and Travel + Leisure Go. Wyndham Club and others, backed by the extensive catalog of timeshares within the RCI platform, now allow members to choose various resorts, rather than being stuck at a single one. Using a points style, various tiers of memberships have varying awards, but members get locked into long-term contracts.

To have more lenient and less confusing offerings, TNL now offers Travel + Leisure club, a currently $15 ($19.99 when not on sale) monthly subscription that gives access to trip discounts, private concierge, and curated itineraries. This membership is not contracted and can be canceled at any time. However, this platform still favors more affluent customers who are able to travel more frequently, much like timeshares or travel credit card rewards.

As such, a third service platform was added, TNL Go. The site offers extensive and numerous itineraries for travelers and frequently offers links to join TNL Club. While more of an intermediary between the magazine website and club, perhaps the company will look to establish online booking features similar to Booking.com (BKNG) or Expedia (EXPE). The company also offers the Panorama software platform that enables condominiums, apartments, and/or resorts and other vacation rentals to have their own website platform for bookings.

There are other parts I could discuss, but the gist is that the magazine website drives traffic and the desire to travel, then initial travelers will look at itineraries on the T+L Go site. After enjoying a vacation, those who want to continue traveling or vacationing throughout the year will join T+L Club. Then, the top-tier of earners or retirees with extra income will be the main purchasers of timeshare club memberships. This positive feedback loop allows for the synergies between units that I discussed earlier. Although, one must be considerate of excess spending on the tech platforms, and one consolidated site or membership may be better. I am sure the company will assess this contingency as well.

TNL

TNL

Financials

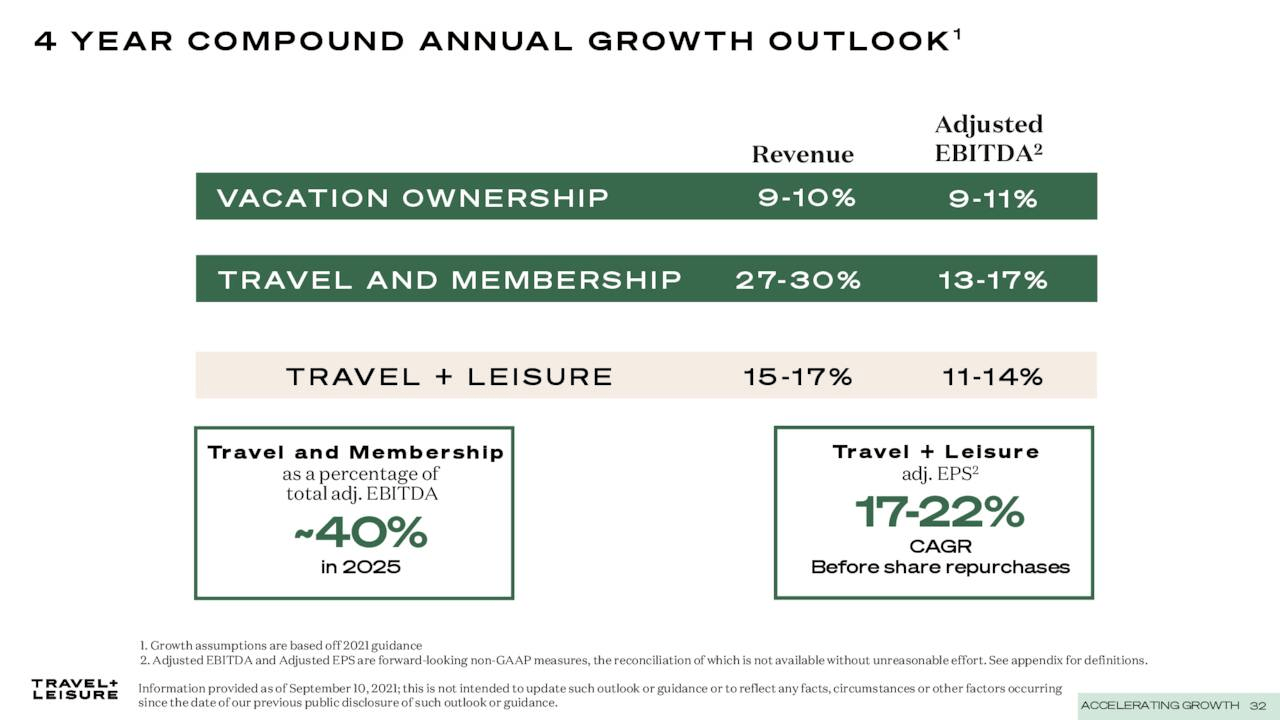

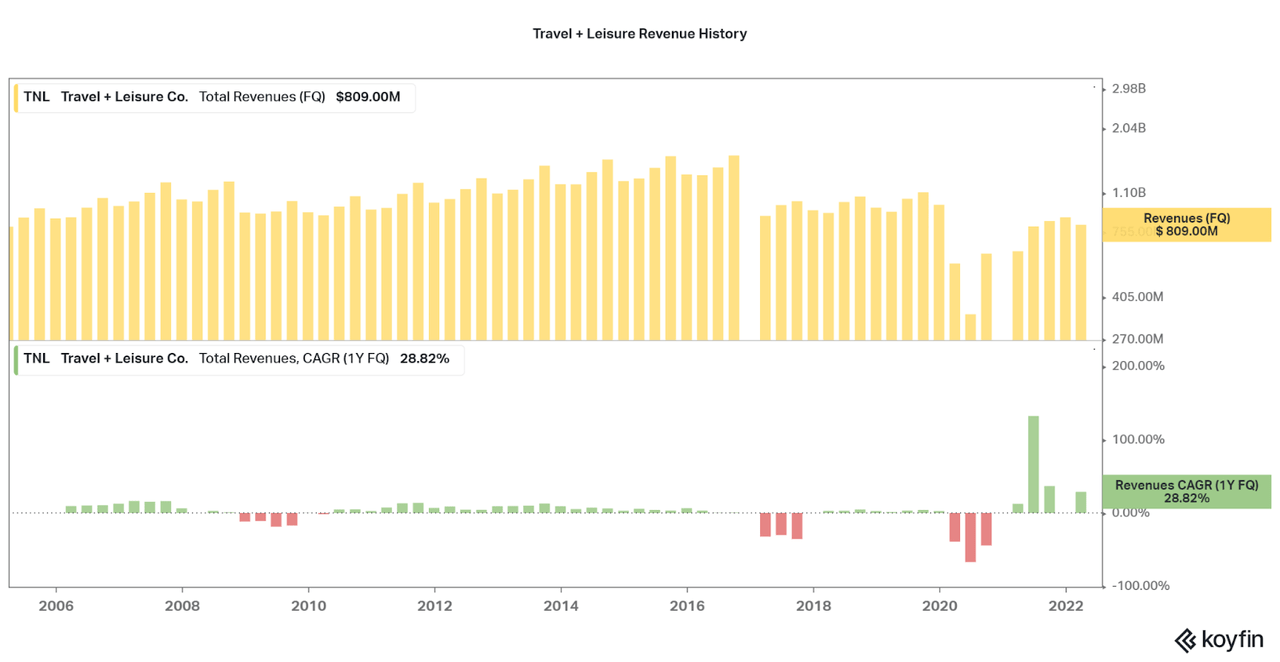

So, how do these changes affect the financials? While the company expects significant growth over the next four years, we can make little insights into whether this is beyond prior performance. So far, revenues have rebounded to slightly less than 2019 revenues, and are less than what the Wyndham business saw on its own prior to merger. However, most travel industry names are still receiving fewer revenues than prior to the pandemic. As such, I believe it will take some time to be able to break down the revenues and growth potential of the company.

For the moment, the driving catalyst will only be a return to pre–pandemic travel levels. Issues with inflation and recessions will also hinder the stock, so the return will likely be slower than expected. However, in the long run, I do not believe the company will return to the revenue growth seen in the 2010-18 period, and will in fact grow faster.

TNL Koyfin

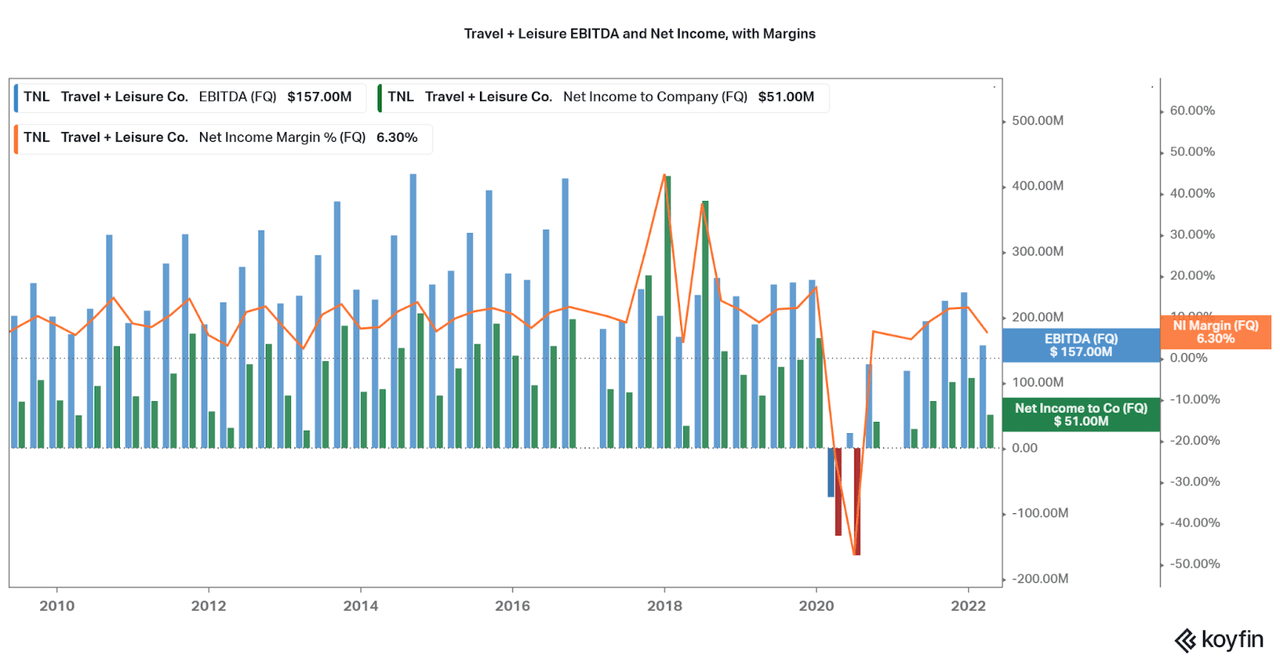

While 2020 was met with steep losses initially, I find that T+L was able to maintain strong profitability during the later stages of the pandemic. In fact, two quarters were negative, but then by 2021, the net income margin returned above 5%, with some quarters hitting 10%. The timeshare industry has a history of slow, but profitable growth, and it seems this pattern allowed for safety into 2021. I also believe the magazine segment remained strong as well, as the desire for travel content did not subside, just the capability to travel; I know I planned out many trips for once I could travel again over the past two years.

Koyfin

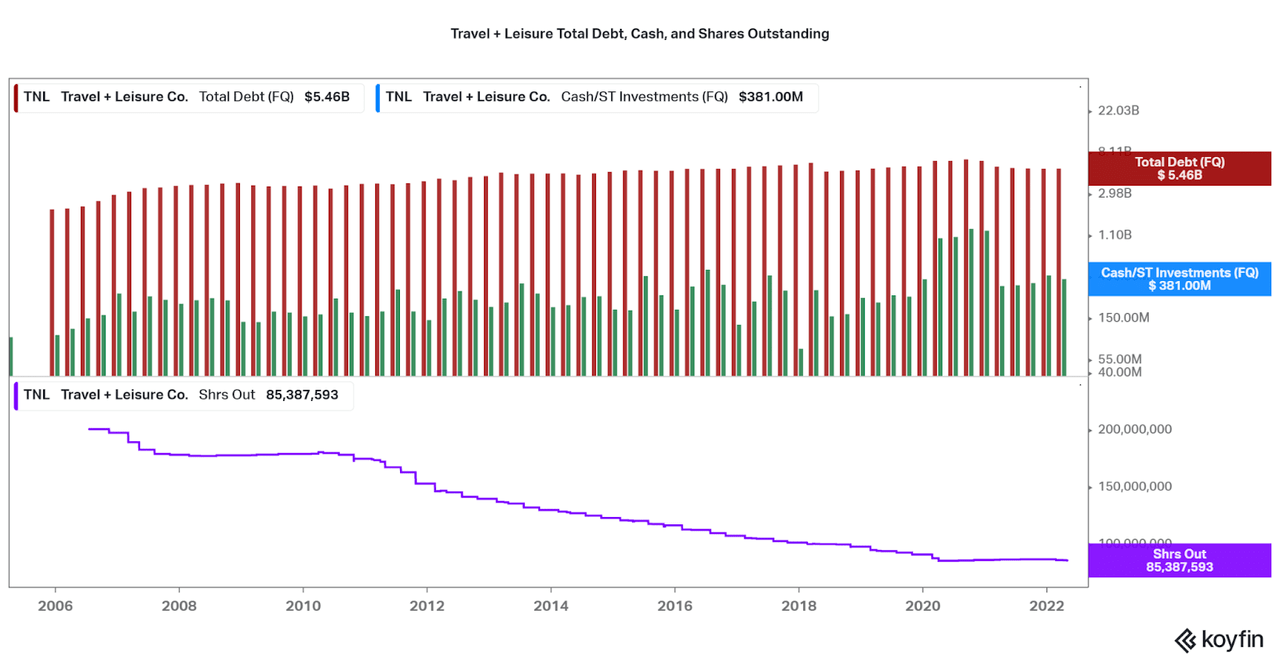

Taking a look at the balance sheet also paints a contrasting picture. While there is significant debt on the balance sheet, cash levels actually improved in 2020/21. I like to see that debt is not increasing as a result of the pandemic, and this may be a positive benefit to the newly merged companies. Further, the company had a history of steadily decreasing the overall share count, and dilution did not occur during the pandemic. While I believe TNL offers a safe balance sheet, I would continue to keep watch along with the rest of the financials as travel returns to normal. There is much uncertainty in the market and economy, and no need to rush into an investment.

Koyfin

Price and Valuation

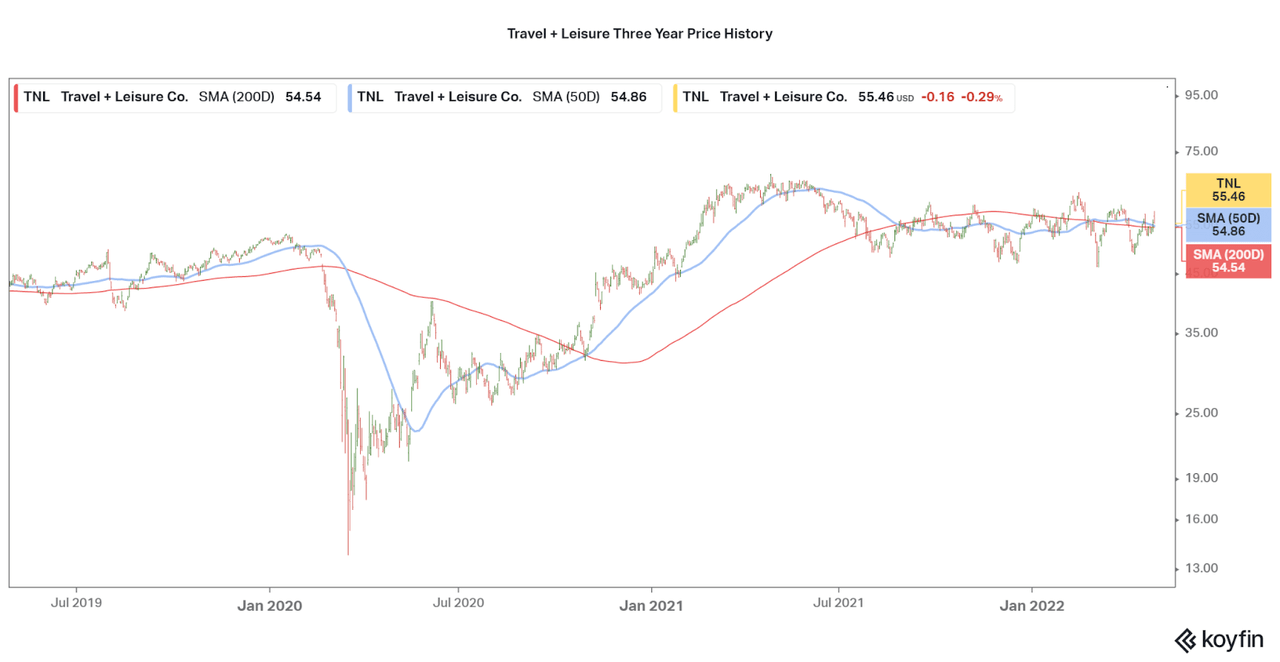

As the company has had a big change with their internal structure, and the pandemic hit at the worst time, TNL‘s share price has failed to reach highs seen prior to the pandemic. There was an initial surge along with valuations last summer, but this quickly fell afterwards, although a holding pattern has emerged between $40 and $60 per share. While it is quite obvious to investors that they should have bought during pandemic lows, we can also look at the valuation of the company as potential support for the investment.

Koyfin

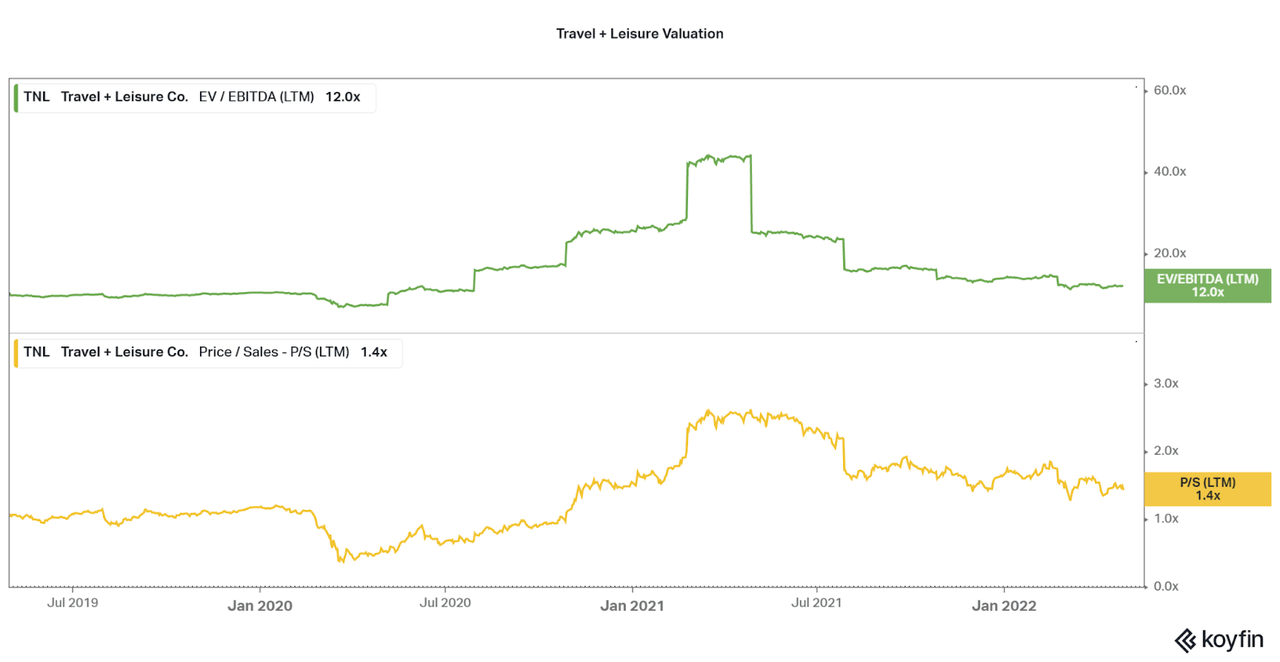

While the price to earnings chart offers little insight and is excluded, the current P/E of TNL is a meager 14.5 (TTM, GAAP). This implies the market is pricing in little growth for the company, even as performance returns. This is highlighted by the EV/EBITDA value of 12.0x, falling steadily since last summer. Further signs of weakness are in the P/S, but due to the lowered revenues, remains above lows of 2019 and 2020. Any favorable revenue growth and maintained profitability will quickly drive the valuation lower. As an investor, it will be important to assess whether values will continue falling, stay the same, or expand. However, I prefer not to gamble, and I would consider the company entering into fair or low valuation territory from here.

Koyfin

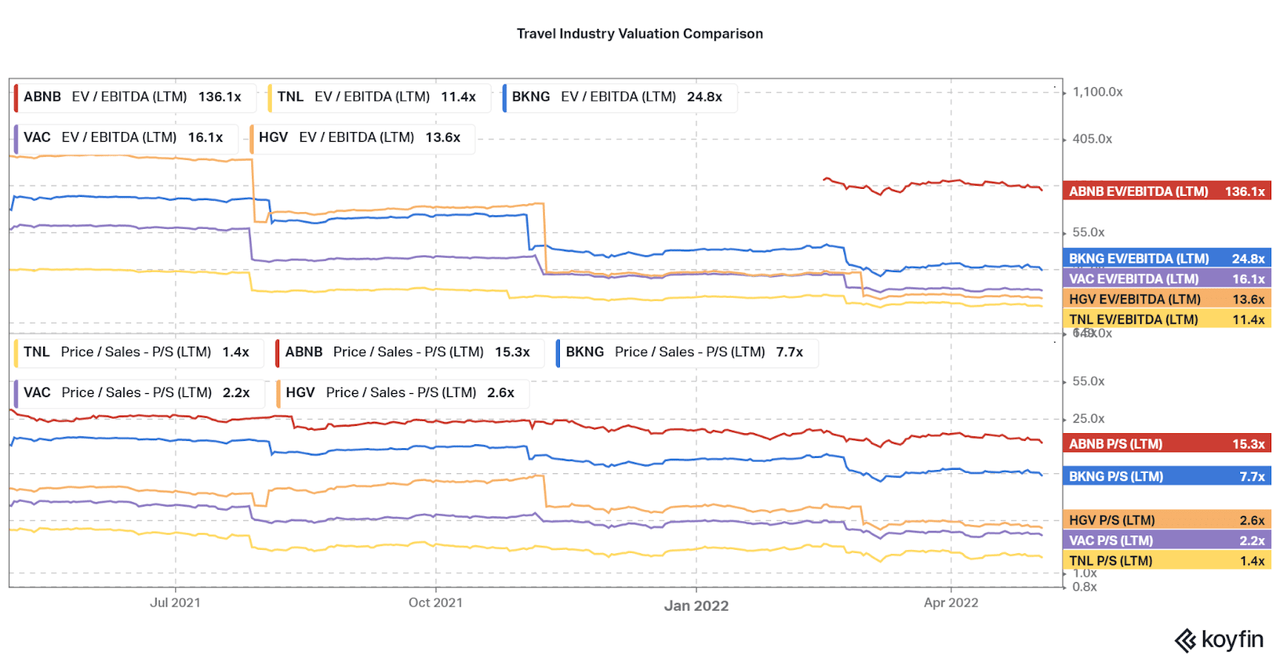

Another way to assess Travel + Leisure is by comparing the valuation to peers. While performance is difficult to assess due to TNL‘s new status, it is plain to see that the company holds a far lower valuation than any peer within the travel industry, even other timeshare or itinerary providers such as Hilton Grand Vacations (HGV) and Marriott Vacations (VAC). Meanwhile, booking platforms such as Booking.com and Airbnb hold far higher valuations, even as their own growth rates falter. In this current market era, profitable, stable growth will hold a higher valuation, and this favors T+L as tourism returns in time. Of course, all of these names offer slightly different exposure to the market, and must also be assessed for their own merits.

Koyfin

Conclusion

I believe that Travel + Leisure is one of the more unique stocks in the travel industry, and certainly worth consideration at current valuations and upside potential. While worries about further COVID variants, international travel, and even a recession weigh heavy on the outlook, T+L seems to be performing well now that they are combined with Wyndham Destinations. Also, a rebranding of timeshares, and a reduction in their negative qualities (such as non-cancelable contracts), will allow for a resurgence of the industry better than with peers. The newly established feedback loop of creating desire to travel (magazine/website), providing travel planning and concierge service (T+L Club), and then finally the higher value timeshare ecosystem for those who want the full experience, is a positive catalyst for the company‘s potential. While I will be sitting on the sidelines for the moment, I may see an opportunity to buy if the share price goes down much further.

Thanks for reading, let me know what you think in the comments.

[ad_2]

Source link

More Stories

National Park Adventures: Find Hidden Gems in the Wild

National Park Adventures: Explore Majestic Landscapes

Journey into the Wild with National Park Adventures