[ad_1]

ajr_photographs/iStock by means of Getty Pictures

Investment decision thesis

Booking Holdings’ (NASDAQ:BKNG) benefits for Q1 FY12/2022 highlighted favourable management commentary about gross bookings in April 2022 achieving pre-pandemic degrees. Inspite of these constructive information, the shares have reacted tiny. We believe the cost of living crisis will strike holiday getaway conduct negatively into H2 FY12/2022, slowing the speed and scale of recovery. With consensus estimates seeking far too bullish, we price the shares as neutral.

Critical financials and consensus earnings estimates

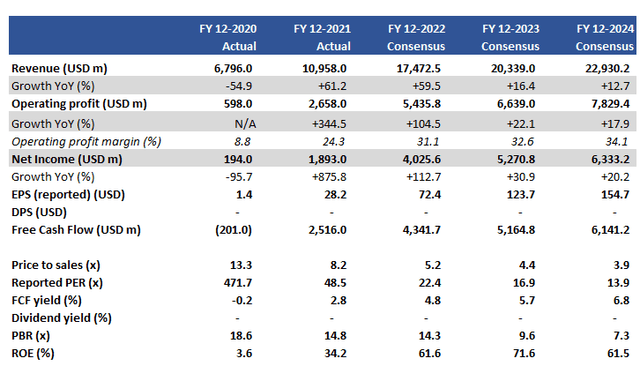

Crucial financials and consensus earnings estimates (Firm, Refinitiv)

Our aims

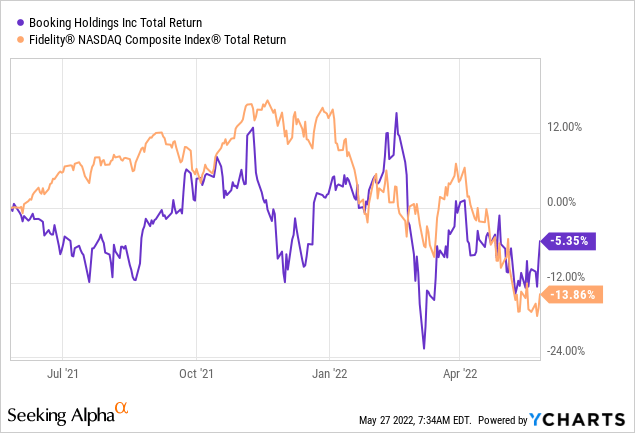

The loosening of travel limitations article COVID19 need to herald a period of time of robust demand from customers for Reserving Holdings, coming in the variety of pent-up demand from customers from both equally business enterprise and leisure vacationers. Booking’s shares have outperformed the NASDAQ Index in the final 12 months but not by a really significant margin.

In this piece we want to assess the pursuing:

- Assess the amount of present-day desire for vacation, and its outlook presented the softer outlook in buyer sentiment.

- Revisit our provide recommendation from March 2021, taking into account consensus estimates for the next two yrs.

We will choose every just one in change.

Demand remains delicate

The summary we arrive to is that regrettably for the vacation marketplace, need at this time stays softer than hoped. With lots of components of the planet going through a price of living disaster, and the Russian invasion of Ukraine ensuing in a key boost in the price of fundamental items, we imagine this will have a major detrimental affect on the long term recovery of leisure journey.

We come across data disclosed by the UNWTO (United Nations Globe Tourism Firm) as one indicator of the tourism industry’s well being. Whilst the knowledge obtainable is not thoroughly up to date, their Tourism Recovery Tracker spotlight beneficial knowledge YoY in the restoration in vacation sentiment and quick-phrase rental demand for April 2022. Even so, what continues to be deeply unfavorable YTD assortment from true air reservations down 70% YoY, resort bookings down 69%, and very low resort occupancy charges at 58%. There is proof of restoration in other places, for occasion, Japan has observed a 1,185% YoY boost in abroad tourists in April 2022 but this continues to be down 95% from the ranges noticed in pre-pandemic April 2019. The hurdle charges versus pre-COVID19 degrees are exceptionally higher.

The hazard from climbing prices will effect shoppers as properly as the hospitality trade alone, which is also struggling with increasing enter costs in power, meals and wine, and payroll. A probable fall in supply will also be a adverse for vacation web pages as merchant volumes start off to fall off.

Company vacation appears to be faring greater. American Convey Worldwide Company Vacation (which is merging with SPAC Apollo Strategic Progress Money (APSG)) commented that the to start with three weeks of April 2022 saw transactions achieve 72% of 2019 degrees. There seems to be much better momentum right here vs . leisure with the corporate entire world returning to journey. The difficulty listed here would be that with enterprise travel earning up all around 20% of the total market, the market can only be actually saved with leisure volumes returning.

The consensus seems much too bullish (once more)

In our prior remark in March 2021, we felt that consensus forecasts were being much too bullish, specifically for organization vacation recovery and we rated the shares as a market. This time, we imagine consensus is as soon as all over again becoming way too bullish for the following explanations.

For FY12/2022, we think the ‘bumper’ summer of desire is not likely to be sustainable. In the effects get in touch with for Q1 FY12/2022, administration commented that at Scheduling.com gross bookings for the summer period ended up around 15% higher than at the similar level in 2019 – but a significant percentage of these bookings were cancelable and the scheduling window had recovered (people today reserving in advance had been related to pre-pandemic concentrations, for this reason have sufficient time to terminate). The crucial issue is around how sustainable this desire profile is compared to a one particular-time restoration from pent-up demand. With the current macro environment, we can not envisage a continuous restoration that spills above into H2 FY12/2022.

What also would seem much too bullish is consensus estimating that the firm’s once-a-year revenues will maintain recording double-digit expansion into FY12/2023 (+16.4% YoY) and FY12/2024 (+12.7% YoY). In the heady times of progress between FY2015-2019, the enterprise grew product sales by 13.% YoY CAGR – we discover it really really hard to feel that it can match such development fees thinking of inflationary price tag pressures, falling standards of living, and greater hurdles YoY.

The two present areas of weakness for the corporation are the Asia current market and very long-haul worldwide vacation. With travel limitations becoming lifted, there will be a surge in desire but the difficulty will be the price of restoration in ADR (typical everyday costs) in accommodation which will acquire some time. Also, in the earth of distant do the job, the require for enterprise vacation has fallen which will have a long lasting effects on global travel quantity.

Scheduling Holdings could intention to increase market share to accelerate topline advancement, but we believe that the total industry pie demands to grow for the organization to accomplish for every consensus estimates. This does not glance very likely to us at this place.

Valuations

On consensus estimates (in the table earlier mentioned in the Important Financials part) the shares are buying and selling on a cost-free hard cash move yield of 5.7% for FY12/2023. This is an beautiful generate and would area the shares in the undervalued category. Having said that, with consensus estimates showing far too bullish we consider a much more practical generate to be all around 4%. Therefore, the shares seem more relatively valued.

Challenges

Upside danger arrives from a sustained need recovery in leisure journey as restrictions are lifted and customers begin to allocate paying out on holidays. The organization has witnessed powerful numbers in April 2022, and if this sort of traits keep on the outlook is favourable.

A somewhat swift conclusion to the Russian invasion of Ukraine will guide in lifting customer sentiment as very well as putting some downward pressure on inflation (specially for agricultural foodstuff rates).

Downside possibility comes from the enhance in the price tag of dwelling which prospects to travelers ‘trading down’. The selection of accommodation concentrates on lessen priced stock ensuing in falling ADR and revenues.

A protracted conflict in Europe challenges finding other sovereign countries finding associated, which would spot tension on the European journey industry. The cancellation price may well boost as a end result.

Summary

In spite of encouraging remarks from administration about recent trading, the company’s shares have reacted minor. We place this down to the marketplace examining the risk of a world-wide recession and the detrimental affect this will have on vacation habits. While we expect a recovery for the organization, we believe the tempo and scale will be slower and lesser than current consensus estimates. With current market anticipations getting fairly superior, we now rate the shares as neutral.

[ad_2]

Resource connection

More Stories

National Park Adventures: Find Hidden Gems in the Wild

National Park Adventures: Explore Majestic Landscapes

Journey into the Wild with National Park Adventures